** Originally published in World Economic Forum Agenda on 6 July 2020 **

|

|

|

The COVID-19 pandemic is a tragic health crisis causing irreversible damage to the global economic and financial system. It is also worsening trade restrictions and reducing trade volumes globally. Coupled with the scarcity of financing in general, and trade financing in specific, coronavirus is causing serious damage to developing economies.

Least developed countries (LDCs) are among the hardest hit. Their already fragile economies are facing further challenges, as the value of their exports plummet and their borders are closed to trade and tourism, like most countries worldwide. Local and foreign investments are drying up. Small business revenues and orders have been reduced drastically.

The cost of financial transactions is increasing, as working with financial institutions in LDCs is perceived to be riskier than before. The issuance of letters of credit and other trade finance instruments is becoming difficult, if available at all, and the appetite of correspondent banking is decreasing each day as the crisis unfolds.

Because of this, LDCs are seeing a rapid depletion of their foreign reserves, and their financial institutions are facing a shortage of liquidity. The persistence of this situation could lead LDCs to drift further away from global value chains and to be left out of the international trade system.

Access to trade finance was already an issue prior to the pandemic. The global trade finance gap is estimated at $1.5 trillion and it is mostly impacting small and medium-sized enterprises in developing countries. Over 50% of requests for financial support to trade are rejected.

The actions that were being taken to reduce the global trade finance gap – including policy advancement, technical assistance, capacity building, regulatory reform and increased financing – are more important now than ever before, to ensure that the world’s most vulnerable countries are not further entrenched in economic inequality because of the pandemic.

What is being done?

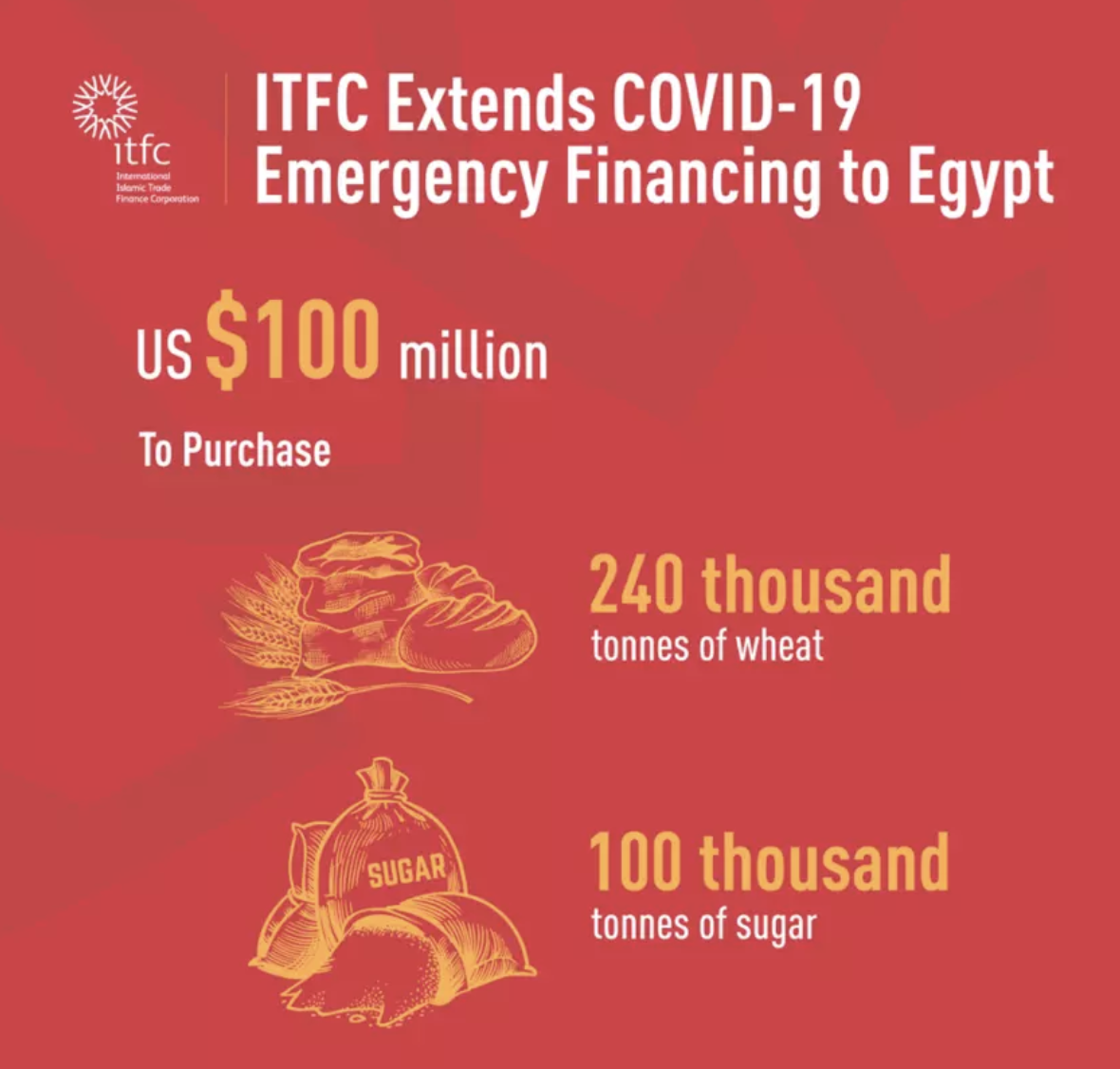

Multilateral development banks (MDBs) have launched immediate responses and financial support amounting to more than $200 billion for emerging and low-income countries. For instance, the Islamic Development Bank Group has launched an initial 3Rs, as in “Respond, Restore, Restart”, for a total $2.3 billion to support Organization of Islamic Conference (OIC) countries at different stages of the recovery trajectory. More specifically, trade finance is a pivotal component of support to the private sector as acknowledged by the G20 Ministers of Finance and Central Bank Governors at their April 2020 meeting. In addition the WTO and MDBs committed to support trade finance The International Islamic Trade Finance Cooperation (ITFC) has pledged an initial $300 million response package to support strategic health, food and energy trade flows and further grant elements to build the capacity of medical personnel and laboratories in OIC countries.

In addition to finance itself, technical assistance programmes are enabling LDCs to build their capacity to provide trade finance. For example, a successfully piloted international trade e-learning programme developed by ITFC and the International Chamber of Commerce is now being provided digitally to financial institutions in LDCs, with the support of the Enhanced Integrated Framework (EIF) and several multilateral development banks and major commercial banks. MDBs are also working together to overcome trade finance barriers, including compliance challenges.

For example, ITFC and EIF are working together in The Gambia, at an initial stage, to test the eradication of aflatoxin from groundnuts – a major export barrier. Most of the resulting harvest was compliant with European Union and FAO-WHO sanitary requirements. The aflatoxin-free and processed groundnuts have the potential to sell at a price 40% higher than in 2016.

ITFC has also developed a programme to support SMEs and their entire ecosystem, including government agencies and financiers, with a West Africa pilot launch in Burkina Faso in 2018. The programme provides access to finance, capacity building and advisory services.

Alongside an $8 million line of finance provided by ITFC to Coris Bank, the Burkina Faso project worked with 60 SMEs whose applications for financing had previously been rejected by the bank. The project resulted in $1.3 million in additional financing granted by the partner bank to 11 SMEs. The programme is now being scaled up in Senegal and soon to other West African countries.

What more needs to be done

International trade and investment are a pivotal component in future economic and financial recovery plans. More specifically, trade finance is a critical factor in the functioning of supply chains and in the creation of employment opportunities. Technical assistance and capacity building related to trade finance will be required to build LDCs resilience. It is also important to fill the trade finance gap, including attracting non-traditional investors to invest in trade finance asset classes. The development of specialized investment vehicles and funds could provide institutional investors with the needed trade finance expertise and transaction portfolios.

All future actions should echo the call for the international community to provide financial commitments, debt restructuring and relief, and stimulus packages supporting SMEs in LDCs. It is also critical to ensure that COVID-19-related trade and investment restrictions remain transparent, temporary, targeted and limited. The international trade system and multilateralism should be preserved and strengthened. The ongoing reforms should proceed, while including new international trade policy priorities like e-commerce. International trade is essential to save lives and livelihoods.

But, we also need to go further. Navigating the treacherous waters ahead is going to require a rewiring of the international community’s approach to supporting LDCs to access international trade. LDC governments and financial institutions need liquidity and trade finance to ensure their ability to participate in what currently remains of international trade. It is important to strengthen investment and maintain resilient and sustainable supply chains, including logistics and transport.

Expertise and policy support are critical to enable LDCs to make informed decisions and institutional reforms that are needed right now. Technical assistance programmes also need to be maintained where possible, particularly those that can be delivered digitally.

The situation may seem dire but crises also have the potential to bring out the best in human cooperation. Let’s ensure that COVID-19 spurs us to rebuild our economic and financial systems in ways that are more just and sustainable, particularly for the world’s LDCs. It is imperative to support the most vulnerable and to leave no one behind.

If you would like to reuse any material published here, please let us know by sending an email to EIF Communications: eifcommunications@wto.org.